Building a good credit history is one of the most powerful things you can do for your financial future. Whether you live in Nigeria, Kenya, South Africa, Ghana, or Uganda, your credit history determines how banks, lenders, and even employers view your reliability.

A good credit history can open doors to better loan terms, higher limits, business financing, job opportunities, and even cheaper insurance. Yet many students and young working-class Africans don’t understand how credit history works—or how to build it properly.

In this article, we’ll walk you through everything you need to know about building a good credit history step-by-step, using clear and simple English. Even a 10-year-old can understand these steps!

Table of Contents

-

What is Credit History?

-

Why Credit History Matters in Africa

-

How Credit Bureaus Work in Nigeria, Kenya, Ghana, Uganda & South Africa

-

Step-by-Step Guide to Building Good Credit History

-

Step 1: Understand How Credit Works

-

Step 2: Start with Small Credit Accounts

-

Step 3: Always Pay on Time

-

Step 4: Keep Credit Utilization Low

-

Step 5: Monitor Your Credit Report Regularly

-

Step 6: Avoid Too Many Loan Applications

-

Step 7: Keep Old Accounts Open

-

Step 8: Diversify Your Credit Responsibly

-

Step 9: Correct Any Errors on Your Credit Report

-

Step 10: Stay Consistent Over Time

-

-

Benefits of Building Good Credit History

-

Mistakes to Avoid When Building Credit

-

Comparison: Building Credit in Africa vs Other Countries

-

Real-Life Examples: How Young Africans Built Good Credit

-

Summary Table: 10 Steps to Building Good Credit History

-

15+ Frequently Asked Questions

-

Conclusion and Call to Action

What is Credit History?

Credit history is a record of how you borrow and repay money. It shows your past and current debts, credit cards, mobile loans, payment habits, and how responsible you are with credit.

When you apply for a loan or credit card, lenders check your credit history to see if you are trustworthy.

Your credit history is stored in a credit report, which is managed by a credit bureau (also called a Credit Reference Bureau or CRB). These bureaus collect data from banks, mobile loan apps, SACCOs, and other lenders.

Key parts of your credit history include:

-

The number of loans you’ve taken.

-

How often you pay your debts on time.

-

Any missed or late payments.

-

The total amount of credit you use.

-

The length of your credit accounts.

-

Types of credit you use (e.g., personal loans, credit cards, car loans).

-

Public records such as defaults or legal actions.

In simple terms: Your credit history tells your financial story. It helps lenders answer one question: “Can we trust you with money?”

Why Credit History Matters in Africa

In Africa, having a good credit history is becoming more and more important. With the growth of mobile money, online lending, and digital banking, your credit history follows you everywhere.

Here’s why it matters:

-

Easier Loan Approvals

-

Banks and microfinance institutions rely on credit history to decide whether to give you a loan.

-

-

Better Loan Terms and Lower Interest Rates

-

With good credit, you can get lower interest rates and larger loan limits.

-

-

Business Opportunities

-

Entrepreneurs and freelancers can access business loans more easily if they have solid credit records.

-

-

Employment and Rental Applications

-

Some employers and landlords check your credit report to gauge your responsibility.

-

-

Financial Freedom

-

A good credit history helps you build trust with financial institutions, making it easier to reach your goals—buying land, a car, or paying for school.

-

In Nigeria, Kenya, Ghana, and South Africa, banks use CRB data to approve mobile loans (like M-Shwari, Carbon, FairMoney, or Branch). This trend shows that credit reputation is now a core part of your financial life.

How Credit Bureaus Work in Africa

Credit bureaus are the organizations that collect and store your financial data. They track how you use credit and share this information with lenders when requested.

Major credit bureaus in Africa:

-

Nigeria: CRC Credit Bureau, CreditRegistry, FirstCentral.

-

Kenya: TransUnion, Metropol, Creditinfo.

-

South Africa: Experian, Compuscan, TransUnion SA.

-

Ghana: XDS Data, Dun & Bradstreet.

-

Uganda: Compuscan Uganda, Metropol CRB Uganda.

These bureaus maintain your credit report and compute your credit score — a number that reflects how good or bad your credit history is.

Typical credit score ranges (example):

-

300–550: Poor credit (high risk)

-

551–650: Fair credit

-

651–750: Good credit

-

751–850: Excellent credit

Your goal is to build and maintain a “Good” or “Excellent” credit score.

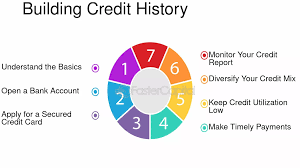

Step-by-Step Guide to Building Good Credit History

Let’s go through each step carefully.

Step 1: Understand How Credit Works

Before you can build credit, you must understand it. Credit simply means borrowing money now and repaying it later, often with interest.

Your credit history grows when you borrow and repay responsibly. If you never use credit, there is no record to prove you’re trustworthy.

So, the first step is to understand that credit is a tool—and like any tool, it can help you or harm you.

Good credit use:

-

Borrow small, repay on time.

-

Keep records of all transactions.

-

Monitor your loans and limits.

Bad credit use:

-

Borrow too much.

-

Pay late or skip payments.

-

Ignore your reports or alerts.

Think of your credit as your financial reputation. Build it carefully, just like you’d build your personal reputation.

Step 2: Start with Small Credit Accounts

If you’re new to credit, start small. Lenders are more comfortable giving small loans to beginners.

Examples of starter credit options:

-

Mobile loans – e.g., M-Shwari (Kenya), Carbon (Nigeria), FairMoney, or Branch.

-

Store credit or buy-now-pay-later plans – e.g., paying for electronics in instalments.

-

Student loans or educational financing.

-

Secured credit cards – cards backed by a small cash deposit.

When you take these small loans and repay them on time, it signals to lenders that you’re reliable.

Pro tip: Don’t borrow more than 30% of your income. Stay small but consistent.

Step 3: Always Pay on Time

This is the most important rule of building good credit. Always pay your loans, bills, or credit card balances on time.

Late payments are recorded as negative entries in your credit report, which can lower your credit score.

Tips to stay on time:

-

Set reminders or calendar alerts for payment dates.

-

Use auto-pay if possible.

-

Pay at least the minimum amount due before the deadline.

-

Communicate with your lender if you face financial difficulties.

Even one late payment can harm your score. Consistency is key.

Step 4: Keep Credit Utilization Low

Credit utilization means how much of your available credit you’re using.

Example: If you have a ₦100,000 credit limit and you’re using ₦80,000, your utilization is 80%—which is too high.

Try to use less than 30% of your available credit. High usage makes you appear risky.

Good practice:

-

If your limit is ₦100,000, keep your usage below ₦30,000.

-

If you often use more, ask for a higher limit once your history improves.

This shows lenders that you manage credit responsibly.

Step 5: Monitor Your Credit Report Regularly

Your credit report can have errors. Monitoring it helps you detect problems early.

You’re entitled to one free credit report per year from each licensed credit bureau in your country.

What to check for:

-

Wrong personal details.

-

Duplicate accounts.

-

Paid loans still showing as unpaid.

-

Loans you didn’t take (possible identity theft).

If you spot an error, file a dispute with the credit bureau. They must correct it within a few weeks.

Step 6: Avoid Too Many Loan Applications

Each time you apply for a loan or credit card, the lender checks your credit report. These checks are called “hard inquiries.” Too many of them in a short time can reduce your score.

Smart tip:

-

Only apply for credit when you really need it.

-

Space out your applications by several months.

Avoid “loan shopping” across multiple lenders at once—it signals desperation.

Step 7: Keep Old Accounts Open

The length of your credit history is another key factor in your credit score. The longer you’ve managed credit responsibly, the better.

Even if you don’t use an account often, keep it open and in good standing. Closing old accounts can shorten your credit history and lower your score.

If the account has no fees, keep it active by making small transactions occasionally.

Step 8: Diversify Your Credit Responsibly

Lenders like to see that you can handle different types of credit—like small loans, credit cards, and installment payments.

But this doesn’t mean you should take multiple loans at once. The goal is variety + discipline.

For example:

-

Have one mobile loan + one small installment plan + one savings-linked loan.

-

Manage them well to show you can handle multiple obligations.

This diversity helps you build a strong credit profile.

Step 9: Correct Any Errors on Your Credit Report

If your report shows a mistake, don’t panic. You have the right to correct it.

Steps:

-

Get your full credit report.

-

Identify the error (wrong loan, wrong payment status, etc.).

-

Gather evidence (receipts, screenshots, bank statements).

-

File a dispute with the credit bureau.

-

Follow up until it’s corrected.

This process can take 21–30 working days, depending on your country’s CRB regulations.

Fixing errors is essential for keeping your history clean and accurate.

Step 10: Stay Consistent Over Time

Credit history is built slowly. There are no shortcuts.

It can take 6–12 months of responsible behaviour to start seeing real improvement in your score.

Stay consistent by:

-

Paying every bill and loan on time.

-

Avoiding unnecessary debt.

-

Keeping your credit utilization low.

-

Reviewing your reports regularly.

Remember: Good credit is built by habit, not by luck.

Benefits of Building Good Credit History

Having a strong credit history brings several benefits:

| Benefit | Explanation |

|---|---|

| Easier access to loans | Lenders are more likely to approve your applications. |

| Lower interest rates | Good credit = lower risk = cheaper loans. |

| Higher credit limits | You may qualify for larger borrowing limits. |

| Better job and housing opportunities | Some employers and landlords check credit records. |

| Emergency financial support | You can access credit quickly in emergencies. |

| Peace of mind | You won’t worry about rejections or hidden debts. |

Mistakes to Avoid When Building Credit

-

Missing payments – Even one late payment can damage your record.

-

Borrowing too much – Stay below 30% of your credit limit.

-

Closing old accounts – This shortens your credit history.

-

Ignoring your report – Mistakes can remain unnoticed.

-

Falling for “quick fix” scams – No one can erase your credit overnight.

-

Applying for too many loans – Creates the impression you’re desperate.

-

Not communicating with lenders – If you struggle to pay, talk to them early.

Avoid these traps to maintain a healthy credit journey.

Comparison: Building Credit in Africa vs Other Countries

| Region | Credit System | How People Build Credit |

|---|---|---|

| Africa (Nigeria, Kenya, Ghana, etc.) | Emerging systems via CRBs, mobile money data, and digital lenders. | Start with mobile loans, microfinance, or salary accounts. |

| United States/UK | Long-established systems with credit cards and FICO scores. | Use credit cards, mortgages, student loans. |

| Asia (India, Philippines) | Mix of traditional banking and digital lending. | Use mobile lending apps + savings-linked loans. |

Insight: Africa’s digital lending revolution means your mobile phone can help you build credit history. Even small transactions count.

Real-Life Examples

Example 1: A Kenyan Student Builds Credit

Faith, a 23-year-old student, started with a small M-Shwari loan of KSh 500. She repaid it early, borrowed slightly more next time, and continued the cycle. After one year, she had a clean record and was approved for a KSh 50,000 loan to start a small business.

Example 2: A Nigerian Worker Improves His Credit

Chidi had defaulted on a microloan years ago. He later paid it off, disputed the wrong “unpaid” record with the bureau, and started using a secured credit card. Within 9 months, his credit score moved from poor to good.

Example 3: A Ghanaian Freelancer Diversifies Credit

Ama used a small phone financing plan and a savings-linked loan from her SACCO. She kept utilization below 25% and paid early. This diversity of credit helped her build a solid score within a year.

Summary Table: 10 Steps to Building Good Credit History

| Step | Action | Goal |

|---|---|---|

| 1 | Understand how credit works | Know what affects your credit score |

| 2 | Start small | Build a foundation safely |

| 3 | Pay on time | Show reliability |

| 4 | Keep credit usage low | Prove financial discipline |

| 5 | Monitor your report | Catch errors early |

| 6 | Limit loan applications | Avoid red flags |

| 7 | Keep old accounts open | Lengthen credit history |

| 8 | Diversify credit types | Strengthen your profile |

| 9 | Fix errors quickly | Maintain accuracy |

| 10 | Stay consistent | Build lasting trustworthiness |

Frequently Asked Questions (FAQs)

1. What is a good credit score in Africa?

Usually, 650 and above is considered good, while 750+ is excellent.

2. How long does it take to build a good credit history?

It can take 6–12 months of consistent, responsible credit use.

3. Can students build credit?

Yes. Start with small mobile loans, student credit cards, or savings-linked loans.

4. What happens if I miss one payment?

A single missed payment can drop your score by 50–100 points. Always pay on time.

5. How can I check my credit report?

Visit your local credit bureau website (e.g., TransUnion, Metropol, CRC Credit Bureau).

6. Can I build credit without a loan?

Not easily. Credit is built by borrowing and repaying. But paying utility or rent through registered systems may help.

7. Does mobile money help credit?

Yes. Many digital lenders use mobile money repayment data to assess your creditworthiness.

8. Should I close old credit accounts?

No. Keep them open to maintain a longer credit history.

9. What hurts my credit the most?

Late payments, defaults, and applying for too many loans at once.

10. Does checking my credit lower my score?

No. Checking your own report is a “soft inquiry” and does not harm your score.

11. Can I fix bad credit?

Yes. Pay off your debts, dispute errors, and build positive history going forward.

12. What’s the difference between credit report and credit score?

A report is your full financial record; a score is the number summarizing it.

13. How can I increase my score fast?

Pay off debts, make payments early, and correct errors.

14. Is there a way to build credit without a job?

Yes. Use secured cards, or borrow small amounts and repay through savings accounts.

15. Can I build credit in more than one country?

Yes, but each country’s credit bureaus are separate. You must build credit history locally.

16. Why is credit important for young people?

Because it helps you access financial opportunities early—like business loans, cars, or education finance.

Conclusion

Building a good credit history is not just for the rich—it’s for everyone who wants financial freedom. Whether you’re a student in Kenya, a worker in Nigeria, or a freelancer in Ghana, your credit history can make or break your financial dreams.

To recap, here’s the golden formula:

Borrow small. Repay early. Monitor regularly. Stay consistent.

Building good credit takes time, but every payment and positive action counts. Start today—your future self will thank you.