Money can either be your best helper or your biggest problem. Many people earn well but still struggle because of poor money management habits—spending too much, saving too little, or living from paycheck to paycheck.

The good news? You can fix it.

In this step-by-step guide, you’ll learn how to identify bad financial habits, replace them with smart ones, and build a plan that works for your life. We’ll use clear, simple English and real African examples to make every lesson practical and easy to follow.

What Is Poor Money Management?

Simple Definition

Poor money management means not controlling how your money comes in and goes out. It’s when your spending, saving, and investing are unplanned, careless, or emotional.

You may be earning money, but if you don’t manage it well, it will always “disappear.”

Signs You Have Poor Money Management Habits

Here are clear signs that your money habits need fixing:

-

You spend all your salary before month-end.

-

You have no savings or emergency fund.

-

You rely on loans or friends for small expenses.

-

You buy things you don’t need.

-

You don’t track your income or expenses.

-

You don’t have a budget.

-

You don’t invest or think about the future.

If you relate to even two of these, you likely have poor money management—but don’t worry, we’ll fix that.

Why Money Management Is So Important

1. It Gives You Control Over Your Life

When you manage your money, you control your choices. You can say “yes” to what matters and “no” to wasteful spending.

2. It Reduces Stress and Anxiety

Financial stress is one of the biggest causes of worry today. Good management gives peace of mind because you always know where your money is going.

3. It Builds the Foundation for Wealth

You can’t grow wealth without first managing what you have. Smart management leads to savings, investments, and financial freedom.

4. It Helps You Handle Emergencies

When emergencies happen, your planning helps you survive without debt or panic.

5. It Creates Financial Discipline

Money management teaches patience, responsibility, and consistency—the three pillars of success.

Common Poor Money Management Habits

Before we fix bad habits, we must know what they look like.

1. Living Paycheck to Paycheck

Many Africans spend everything they earn monthly. When the salary ends, they borrow or struggle until the next payday.

Fix: Create a budget and set aside savings immediately after earning.

2. Not Tracking Expenses

You can’t control what you don’t measure. Most people don’t know how much they spend on food, data, or transportation.

Fix: Write down every expense or use money apps like Cowrywise, M-Pesa, or TymeBank.

3. Impulse Buying

Buying items you don’t need because they are “on sale” or trending is a common mistake.

Fix: Wait 24 hours before buying non-essential items. Often, the desire fades.

4. No Budget Plan

Without a budget, your money will control you instead of you controlling it.

Fix: Use the 50/30/20 rule—50% for needs, 30% for wants, 20% for savings/investments.

5. Ignoring Debt

Many people ignore debts hoping they’ll disappear. That only makes things worse.

Fix: List all debts, set a payment plan, and stick to it. Pay off high-interest loans first.

6. Lack of Savings Habit

If you spend all your money, you’ll always be broke, no matter how much you earn.

Fix: Save a portion of every income automatically through apps or banks.

7. Not Having Financial Goals

Without goals, you have no direction.

Fix: Set SMART goals—Specific, Measurable, Achievable, Relevant, Time-bound.

8. Relying on One Source of Income

If your job ends today, what happens?

Fix: Develop a side hustle or invest in low-risk options like mutual funds or treasury bills.

9. Not Learning About Money

Financial ignorance is costly.

Fix: Read financial blogs, listen to podcasts, and follow African finance pages for tips.

10. Emotional Spending

Buying things to feel better leads to regret later.

Fix: Find free or cheap ways to relax—walks, reading, or talking to friends.

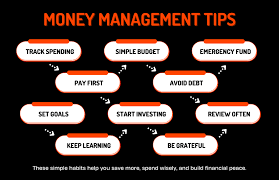

Step-by-Step Guide to Fix Poor Money Management Habits

Here’s how to take control of your finances once and for all.

Step 1 – Acknowledge the Problem

You can’t fix what you don’t admit. Recognize that poor money habits exist.

Write down your top three money problems (e.g., overspending, no savings, debt).

Awareness is the first step toward change.

Step 2 – Track Every Naira, Cedi, Rand, Shilling, or UGX

For one full month, record every single expense.

Use a notebook, spreadsheet, or mobile app.

You’ll be surprised how small purchases add up—snacks, airtime, or data bundles could be stealing your savings.

Step 3 – Create a Realistic Budget

Budgeting is not punishment—it’s freedom. It shows where your money goes.

Simple Budget Formula:

-

50% → Needs (rent, food, bills)

-

30% → Wants (entertainment, clothing)

-

20% → Savings or investments

Adjust based on your income and goals.

Step 4 – Build an Emergency Fund

Before investing, build a safety net. Save 3–6 months of expenses to protect yourself from surprises like job loss or sickness.

Tip: Start small. Even ₦5,000 or KSh 1,000 monthly adds up.

Step 5 – Pay Off Your Debts

Debt eats your income.

List all your debts, interest rates, and payment dates.

Strategy:

-

Pay small debts first for motivation (Snowball method).

-

Or pay high-interest debts first (Avalanche method).

Once debt-free, redirect that money into savings.

Step 6 – Automate Your Finances

Set automatic transfers for savings and bill payments.

Automation ensures discipline and consistency.

Example: Use Cowrywise AutoSave or PiggyVest SafeLock to save monthly without thinking.

Step 7 – Limit Cash and Impulse Purchases

Carry only the cash you plan to spend.

Avoid “window shopping” or scrolling through online stores when bored.

Step 8 – Learn to Delay Gratification

Successful people wait before making financial decisions.

Ask yourself: “Do I really need this right now?”

Patience helps you make smarter money moves.

Step 9 – Set Financial Goals

Write down what you want to achieve in 6 months, 1 year, and 5 years.

Example goals:

-

Save ₦300,000 for a business.

-

Build an emergency fund.

-

Start investing in mutual funds.

Goals give your money direction.

Step 10 – Learn and Improve Constantly

Money management is a lifelong skill.

Read finance books like The Richest Man in Babylon or Smart Money Woman.

Follow local money influencers for African examples.

The more you learn, the better you earn and manage.

How Poor Money Management Affects Your Life

1. Constant Stress

Living without savings or plans leads to worry every month.

2. Debt Trap

When you depend on loans for survival, you’re always behind.

3. Missed Opportunities

Without savings, you can’t invest or take advantage of good deals.

4. Broken Relationships

Money problems cause arguments in families and friendships.

5. Poor Quality of Life

You end up working harder but achieving less because of poor planning.

Benefits of Fixing Poor Money Habits

1. Financial Freedom

You no longer live in fear of “month-end broke syndrome.”

2. Peace of Mind

Knowing your bills and savings are handled brings calmness.

3. Confidence in Decisions

You make smarter choices without guilt or panic.

4. Preparedness

Emergencies won’t destroy your finances anymore.

5. Long-Term Wealth Building

Good habits compound over time, leading to real financial growth.

Tools to Help You Fix Poor Money Management Habits

Budgeting Apps

-

PiggyVest (Nigeria)

-

Cowrywise (Nigeria)

-

M-Pesa (Kenya)

-

TymeBank GoalSave (South Africa)

-

Chipper Cash (Africa-wide)

Expense Tracking Tools

-

Google Sheets

-

Microsoft Excel

-

Wallet App

-

Money Manager

Learning Platforms

-

YouTube finance channels

-

Podcasts like The Money Africa Show

-

Blogs like Smart Money Africa

Real-Life African Examples

Example 1 – The Nigerian Student

Tunde used to spend all his allowance on data and snacks. After tracking his expenses, he cut waste and started saving ₦5,000 monthly. In one year, he had ₦60,000—enough to start a small phone accessories business.

Example 2 – The Kenyan Professional

Grace used to overspend every payday. She started using M-Pesa’s goal feature to automate her savings. Within a year, she paid off her debt and built an emergency fund worth KSh 100,000.

Example 3 – The Ghanaian Couple

Kofi and Ama fought over money until they created a shared budget. Now they plan together, save together, and invest in treasury bills monthly.

The Psychology Behind Poor Money Habits

1. Emotional Triggers

People often spend when stressed or bored. Recognize your emotional triggers and replace them with healthy habits.

2. Social Pressure

Many Africans overspend to impress friends or family. Learn to say no. Real wealth is quiet.

3. Lack of Awareness

Some people simply don’t know better. That’s why financial education is key.

4. Childhood Influence

If you grew up in a home where money was mismanaged, you may repeat those habits—unless you consciously change them.

Comparison: Poor vs. Good Money Management

| Category | Poor Money Management | Good Money Management |

|---|---|---|

| Spending | Impulsive, emotional | Planned and thoughtful |

| Savings | None or inconsistent | Regular and automated |

| Debt | High, ignored | Controlled or zero |

| Budget | Non-existent | Structured monthly plan |

| Goals | Vague dreams | Clear SMART goals |

| Mindset | “I’ll fix it later” | “I’ll start today” |

Summary Table – Key Takeaways

| Step | Lesson | Action Plan |

|---|---|---|

| Identify Problems | Know your bad habits | Write them down |

| Track Spending | Understand where money goes | Record daily expenses |

| Budget | Give your money purpose | Use 50/30/20 rule |

| Save & Invest | Build wealth | Automate savings |

| Learn | Grow knowledge | Follow finance blogs |

| Stay Consistent | Be disciplined | Review progress monthly |

Frequently Asked Questions (FAQs)

Q1: What is poor money management?

A1: It’s when you don’t control how you earn, spend, and save money, leading to waste or debt.

Q2: How do I know if I have bad money habits?

A2: If you always run out of money, have no savings, or borrow often, you likely do.

Q3: Can I fix poor money habits even with low income?

A3: Yes! Start small and stay consistent. Even saving ₦1,000 monthly makes a difference.

Q4: What’s the first step to fixing bad money habits?

A4: Track your expenses and create a realistic budget.

Q5: How can I stop impulse buying?

A5: Wait 24 hours before buying anything unplanned.

Q6: Should I save or pay off debt first?

A6: Do both—start by paying high-interest debts while saving a small amount for emergencies.

Q7: Which app is best for saving in Nigeria or Kenya?

A7: PiggyVest, Cowrywise, and M-Pesa are popular and safe.

Q8: Why do I keep running out of money even with a job?

A8: You may be overspending or not budgeting. Review your expenses weekly.

Q9: How long does it take to build good money habits?

A9: Usually 3–6 months of consistent effort.

Q10: Can I teach my children money management?

A10: Yes. Start early by giving them small budgets and explaining savings.

Q11: What’s the best way to start saving?

A11: Automate savings—let your bank or app do it for you every payday.

Q12: How can I stay motivated to manage money better?

A12: Set goals and celebrate small wins. Seeing progress keeps you going.

Conclusion – Take Charge of Your Financial Future

Fixing poor money management habits is not about perfection—it’s about progress. You don’t need a high income to manage money well. You just need discipline, awareness, and consistency.

Start today:

-

Track your spending.

-

Create a budget.

-

Automate savings.

-

Learn something new about money every month.

Small, smart actions today can transform your financial future.