Your credit worthiness is like your financial reputation — it tells lenders, employers, and even landlords whether they can trust you with money.

If you’ve ever applied for a loan, bought something on credit, or used a mobile lending app, your credit worthiness determines whether you get approved, how much you can borrow, and what interest rate you’ll pay.

Unfortunately, many people in Africa don’t fully understand what credit worthiness means or how to improve it. That’s why this guide was written — in simple, clear English — to help students, workers, and entrepreneurs in Nigeria, Ghana, Kenya, Uganda, and South Africa understand and build strong financial trust.

This is your complete, step-by-step guide to improving your credit worthiness — no technical jargon, no confusion, just actionable steps.

Table of Contents

-

What Is Credit Worthiness?

-

Why Credit Worthiness Is Important

-

How Lenders Measure Credit Worthiness

-

Understanding Credit Scores and Credit Reports

-

Common Reasons for Poor Credit Worthiness

-

Step-by-Step Guide to Improving Your Credit Worthiness

-

Step 1: Check Your Credit Report

-

Step 2: Correct Any Errors

-

Step 3: Pay All Bills on Time

-

Step 4: Reduce Your Debts

-

Step 5: Maintain Older Accounts

-

Step 6: Limit New Credit Applications

-

Step 7: Build Positive Credit History

-

Step 8: Diversify Your Credit Portfolio

-

Step 9: Monitor Your Credit Regularly

-

Step 10: Practice Healthy Financial Habits

-

-

Real-Life Examples: How People Improved Their Credit Worthiness

-

Comparison: Good vs Poor Credit Worthiness

-

Benefits of Being Creditworthy

-

Mistakes That Can Damage Credit Worthiness

-

Tools and Apps That Help Build Credit in Africa

-

How Long It Takes to Improve Credit Worthiness

-

Summary Table: 10 Key Steps to Better Credit Worthiness

-

15+ Frequently Asked Questions (FAQs)

-

Conclusion + Free Credit Improvement Resource

What Is Credit Worthiness?

Credit worthiness means how trustworthy you are when it comes to borrowing and repaying money.

In simple terms, it’s your ability — and willingness — to pay back loans on time.

If lenders believe you will pay back as agreed, you are considered creditworthy. If they think you may default or delay, you are not creditworthy.

Credit worthiness is based on:

-

Your past borrowing behavior.

-

How much debt you currently have.

-

How consistently you repay.

-

Your income stability.

-

Your overall financial management.

Every adult with a Bank Verification Number (BVN) in Nigeria, or a National ID in Kenya or Ghana, has a credit profile that tracks these details through credit bureaus like CRC Credit Bureau, FirstCentral, TransUnion, or Metropol.

Why Credit Worthiness Is Important

Being creditworthy opens doors — it helps you borrow easily, pay less interest, and grow financially.

Here’s why it matters:

-

Easier loan approvals: Banks, SACCOs, and fintech apps trust you more.

-

Better interest rates: You’ll pay less interest because lenders see less risk.

-

Access to higher loan limits: The more trustworthy you are, the more you can borrow.

-

Faster approvals: No need for long waiting or guarantors.

-

Better business opportunities: Investors and partners prefer financially responsible people.

-

Improved job prospects: Some employers check credit before hiring.

-

Peace of mind: You can borrow without fear of rejection.

In short, good credit worthiness = financial freedom.

How Lenders Measure Credit Worthiness

When you apply for a loan, lenders don’t just look at your salary — they look at your credit behavior.

Common factors lenders use:

| Factor | What It Means | Impact |

|---|---|---|

| Credit history | How long you’ve been using credit | Longer is better |

| Repayment history | Whether you pay on time | Most important factor |

| Debt-to-income ratio | How much debt you have compared to income | Lower is better |

| Credit utilization | How much of your available credit you use | Keep below 30% |

| Recent loan applications | Too many new loans can lower trust | Apply sparingly |

| Collateral or guarantees | Backup for repayment | Adds security |

The goal is to show that you are responsible, reliable, and consistent.

Understanding Credit Scores and Credit Reports

Credit Report:

A detailed record of your financial history — including your loans, payments, and defaults — maintained by credit bureaus.

Credit Score:

A number between 300 and 850 that summarizes your credit behavior.

| Score Range | Meaning | Credit Status |

|---|---|---|

| 750 – 850 | Excellent | Very high credit worthiness |

| 650 – 749 | Good | Creditworthy |

| 550 – 649 | Fair | Some risk |

| 300 – 549 | Poor | High risk, may face rejection |

You can check your score from:

-

Nigeria: CRC Credit Bureau, FirstCentral

-

Kenya: TransUnion, Metropol, CreditInfo

-

Ghana: XDS Data, Dun & Bradstreet

-

Uganda: Compuscan, Metropol CRB Uganda

-

South Africa: Experian, TransUnion

Common Reasons for Poor Credit Worthiness

If your credit score or worthiness is low, it’s often due to these reasons:

-

Missed or late loan payments

-

Defaulting on loans or mobile credit apps

-

Too many loans at once

-

Ignoring small debts

-

Not having any credit history at all

-

Errors on your credit report

-

Frequent loan applications

-

Unpaid utility bills reported to credit bureaus

The good news? Each of these can be fixed — and we’ll show you how.

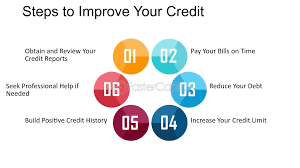

Step-by-Step Guide to Improving Your Credit Worthiness

Step 1: Check Your Credit Report

You can’t fix what you don’t see.

Start by requesting your credit report from any licensed bureau in your country.

In Nigeria, visit:

In Kenya:

Review the report for:

-

Unpaid loans

-

Wrong balances

-

Missed payments

-

Unknown accounts

This helps you understand where you stand and what needs fixing.

Step 2: Correct Any Errors

If you notice any wrong information — like a paid loan showing as unpaid — dispute it immediately.

Contact the credit bureau (CRC, FirstCentral, etc.) and submit proof such as:

-

Payment receipts

-

Clearance letters

-

Bank statements

Bureaus are required by law to fix verified errors within 30 business days.

Step 3: Pay All Bills on Time

Paying on time is the biggest factor in building credit worthiness.

Set reminders or automate payments for:

-

Loans

-

Credit cards

-

Mobile credit (Branch, Carbon, FairMoney, etc.)

-

Utility bills (electricity, internet, DSTV)

Even one late payment can lower your score significantly.

Step 4: Reduce Your Debts

Having too much unpaid debt makes lenders think you’re struggling.

Strategies to reduce debt:

-

Focus on high-interest loans first.

-

Avoid taking new loans until you’ve paid off old ones.

-

Consider a debt repayment plan.

Aim to keep your debt-to-income ratio below 35%.

Step 5: Maintain Older Accounts

Many people close old bank or credit accounts, thinking it helps — but it doesn’t.

The longer your account history, the more reliable you appear.

So even if you’re not using an old account, keep it active with small transactions.

Step 6: Limit New Credit Applications

Each time you apply for a loan, lenders perform a “hard inquiry”, which can lower your score slightly.

Only apply for credit when absolutely necessary.

Too many applications in a short time make you look desperate.

Step 7: Build Positive Credit History

If you’ve never borrowed before, lenders have no data to trust you with.

To build history:

-

Take small loans and repay early.

-

Use mobile credit responsibly.

-

Join a SACCO or cooperative that reports to credit bureaus.

-

Pay utility bills regularly and on time.

Within 6–12 months, your credit report will start reflecting positive patterns.

Step 8: Diversify Your Credit Portfolio

Lenders prefer people who manage different types of credit well.

Example:

-

One personal loan + one credit card + one SACCO loan = diverse portfolio.

It shows you can handle multiple financial products responsibly.

Step 9: Monitor Your Credit Regularly

Make it a habit to check your report every few months.

That way, you can:

-

Catch errors early

-

Track improvements

-

Avoid surprise rejections

Some apps and bureaus even offer free alerts when your credit changes.

Step 10: Practice Healthy Financial Habits

Good credit starts with good money management.

Here’s what to do daily:

-

Budget your income.

-

Save 10–20% monthly.

-

Avoid impulse buying.

-

Track all your expenses.

-

Build an emergency fund (3–6 months of expenses).

Responsible financial behavior naturally improves your credit over time.

Real-Life Examples: How People Improved Their Credit Worthiness

Case 1 – Tunde (Nigeria)

Tunde had a poor credit score of 520 after defaulting on a ₦50,000 loan. He repaid it, requested correction at CRC Bureau, and started using Carbon for small loans he repaid early. Within 8 months, his score rose to 690.

Case 2 – Aisha (Kenya)

Aisha was blacklisted for an unpaid KSh 1,200 M-Shwari loan. She paid it, got clearance from Metropol, and began paying her internet bills early every month. Her score improved from 480 to 720 in one year.

Case 3 – Sipho (South Africa)

Sipho overused his credit card (90% utilization). He reduced it to 25% and started making minimum payments early. His credit score increased by 150 points within 6 months.

Comparison: Good vs Poor Credit Worthiness

| Factor | Good Credit Worthiness | Poor Credit Worthiness |

|---|---|---|

| Loan repayment | Always on time | Frequently late |

| Credit score | 700+ | Below 550 |

| Debt-to-income ratio | Below 35% | Above 50% |

| Loan approval rate | High | Low |

| Interest rate | Low | High |

| Access to credit | Easy | Restricted |

| Financial stress | Minimal | High |

Benefits of Being Creditworthy

| Benefit | Description |

|---|---|

| Easier access to loans | Banks and apps trust you more |

| Lower interest rates | You save money on every loan |

| Higher credit limits | You qualify for bigger amounts |

| Financial confidence | You can plan long-term goals |

| Improved employment chances | Employers value reliable people |

| Better housing opportunities | Landlords trust your payment record |

Mistakes That Can Damage Credit Worthiness

-

Ignoring small loans or mobile debts.

-

Paying late or missing payments.

-

Applying for too many loans.

-

Using too much of your credit limit.

-

Closing old accounts.

-

Not checking your report for errors.

-

Ignoring communication from lenders.

Even small mistakes can have big financial consequences.

Tools and Apps That Help Build Credit in Africa

| Country | Apps/Tools | Use |

|---|---|---|

| Nigeria | Carbon, Branch, FairMoney | Track and repay small loans |

| Kenya | M-Shwari, Tala, KCB M-Pesa | Build credit history |

| Ghana | Fido Money, Bloom Impact | Access digital loans |

| Uganda | Airtel Money, MoKash | Credit from mobile wallets |

| South Africa | TymeBank, Capitec, Experian | Free credit monitoring |

Use these responsibly to grow your financial reputation.

How Long It Takes to Improve Credit Worthiness

Improving credit worthiness is a journey — not an overnight fix.

| Time Period | Expected Progress |

|---|---|

| 1–3 months | Small improvements from on-time payments |

| 4–6 months | Noticeable score increase |

| 7–12 months | Major recovery and new credit opportunities |

| 1+ year | Excellent credit worthiness |

Consistency is the secret — small, regular efforts produce big results.

Summary Table: 10 Key Steps to Better Credit Worthiness

| Step | Action | Result |

|---|---|---|

| 1 | Check your credit report | Know your status |

| 2 | Fix errors | Clean record |

| 3 | Pay on time | Build trust |

| 4 | Reduce debts | Improve balance |

| 5 | Keep old accounts | Longer history |

| 6 | Limit new credit | Fewer inquiries |

| 7 | Build positive history | Increase score |

| 8 | Diversify credit | Show responsibility |

| 9 | Monitor regularly | Stay alert |

| 10 | Practice good habits | Lasting success |

15+ Frequently Asked Questions (FAQs)

1. What is credit worthiness?

It’s your ability and willingness to repay loans responsibly and on time.

2. How can I check my credit worthiness in Nigeria?

Visit CRC or FirstCentral Credit Bureau websites to request your report.

3. Does paying bills improve credit?

Yes. Regular payment of loans, rent, or utility bills builds positive history.

4. Can I improve my credit score if I’m blacklisted?

Yes. Repay your debts, get clearance, and rebuild your profile with small loans.

5. How long does it take to fix bad credit?

Between 6 to 12 months of consistent, responsible behavior.

6. Does checking my credit lower my score?

No. Only lenders’ “hard checks” affect your score slightly.

7. Can mobile loan apps help improve credit?

Yes, if you borrow small and repay early.

8. What happens if I ignore my bad credit?

You may be denied loans, jobs, or business opportunities.

9. Can students build credit?

Yes. Start with small mobile loans or school payment plans.

10. Will paying off debt increase my score?

Definitely — it shows financial responsibility.

11. What if I don’t have any credit history?

Start small. Take low-limit loans or join a SACCO that reports to bureaus.

12. Can errors affect my credit worthiness?

Yes. Even one wrong unpaid loan can drop your score by over 100 points.

13. Who regulates credit bureaus?

The Central Bank of Nigeria (CBN) and similar authorities in other countries.

14. Can employers check my credit?

Yes, especially in financial or security-related jobs.

15. Can I recover from multiple defaults?

Yes, with repayment, dispute resolution, and time.

16. Should I close old accounts?

No. Keep them open — they strengthen your history.

17. How often should I check my credit report?

At least twice a year.

Conclusion

Improving your credit worthiness is one of the smartest financial decisions you can make.

It takes time, discipline, and consistency — but the rewards are worth it. You’ll enjoy easier access to credit, better interest rates, and greater financial confidence.

Remember, every payment, every loan, every decision adds to your story.

Make yours a trustworthy one.

Start today — check your credit report, fix errors, and build a record you can be proud of.