In today’s world, almost everyone borrows money at some point — whether for school, business, rent, or emergencies. Loans can be helpful, but sometimes unexpected situations make it hard to pay them back on time.

Maybe your salary was delayed, your business slowed down, or you faced an emergency. When that happens, you might start worrying about penalties or even blacklisting.

But don’t panic! There is a smart and legal way to handle this situation — it’s called loan repayment extension negotiation.

In this article, we will walk you through everything you need to know about how to negotiate loan repayment extensions step by step — in simple English that anyone can understand.

What Is a Loan Repayment Extension? (Meaning and Simple Explanation)

A loan repayment extension means asking your lender to give you more time to pay back your loan.

It doesn’t mean you are avoiding payment. It simply means you need extra weeks or months to settle your debt without stress.

Think of it like this:

If your teacher gives you more days to submit an assignment, it doesn’t mean you failed — it just means you got more time to do it right.

Key Features of Loan Repayment Extensions

-

You still owe the same loan, but the repayment period increases.

-

Some lenders may charge a small extension fee or interest.

-

You and your lender must agree on the new repayment terms in writing.

-

It helps you avoid default, blacklisting, or harassment.

Example:

If you borrowed ₦50,000 from a loan app in Nigeria and were supposed to repay in 30 days, but you lost your job, you can ask the lender to extend the repayment to 60 or 90 days.

Why People Ask for Loan Repayment Extensions

Before you ask for an extension, it’s important to understand why it’s needed. Many people across Africa — from Nigerian students to Kenyan small business owners — face similar challenges.

Here are common reasons:

-

Salary delay or job loss

-

Medical emergencies or family problems

-

Unexpected business loss

-

School fee or tuition increase

-

Economic inflation or high cost of living

-

Natural disasters or political instability

Requesting a repayment extension shows that you are responsible and willing to pay, not that you are avoiding your debt.

The Importance of Negotiating Loan Extensions the Right Way

Asking for an extension is not a bad thing, but how you do it matters.

If you handle it wrongly, your lender may reject your request or even report you to a credit bureau.

When you handle it correctly, you can:

-

Avoid blacklisting

-

Reduce late penalties

-

Protect your credit score

-

Maintain a good relationship with lenders

-

Reduce stress and embarrassment

That’s why you need a step-by-step guide, which we’ll explain next.

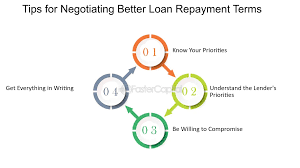

Step-by-Step Guide to Negotiating a Loan Repayment Extension

This is the main part of the article — a detailed, easy-to-follow process for negotiating your loan extension.

Step 1: Stay Calm and Review Your Loan Agreement

Before you contact your lender, read your loan contract carefully.

Look for details like:

-

Repayment period

-

Interest rate

-

Late payment penalties

-

Extension policy (if any)

Knowing your rights and obligations helps you speak with confidence when negotiating.

Pro Tip:

Always keep copies of your loan documents — digital or printed — so you can refer to them anytime.

Step 2: Assess Your Financial Situation

Next, find out why you can’t repay on time and how much time you need.

Ask yourself:

-

How much do I still owe?

-

How much can I pay now?

-

When will I be able to pay the rest?

Write down your monthly income and expenses.

This will help you create a realistic repayment plan to show your lender.

Example:

If your monthly income is ₦100,000 and your loan payment is ₦40,000, but you now earn only ₦60,000, you can propose paying ₦20,000 per month instead.

Step 3: Contact Your Lender Early

Never wait until your loan is overdue before you act.

Contact your lender before the due date.

You can do this by:

-

Email

-

Phone call

-

Mobile app chat

-

Physical visit (for banks or microfinance institutions)

Be polite, respectful, and honest about your situation.

Example Message You Can Send:

Dear [Lender’s Name],

I am writing to request a repayment extension for my loan of ₦50,000 due on [Date].

I recently experienced [brief reason, e.g., job delay], and I will need an extra 30 days to complete repayment.

I am committed to paying my loan in full. Please let me know the process to extend my repayment period.Thank you for your understanding.

Sincerely,

[Your Name]

This kind of message shows maturity and responsibility.

Step 4: Explain Your Situation Honestly

Your lender will likely ask why you can’t repay on time.

Be honest and clear — but don’t over-explain or lie.

Explain your real situation briefly. For example:

-

“My salary payment was delayed.”

-

“I had an unexpected medical expense.”

-

“My business had a temporary cash flow problem.”

Lenders appreciate honesty and are more likely to help if they believe you’re sincere.

Step 5: Propose a New Repayment Plan

Don’t just ask for “more time.” Suggest a clear repayment schedule.

For instance:

-

“Can I pay ₦10,000 weekly for the next five weeks?”

-

“Can we extend my repayment to 90 days with smaller payments?”

This shows initiative and helps your lender see you as a responsible borrower.

Step 6: Negotiate the Terms Professionally

Negotiation means both sides agree on new conditions.

Here’s what you can negotiate:

-

Extra time (e.g., 30–90 days more)

-

Lower interest rate or temporary freeze

-

Waiver of penalties

-

New payment schedule

Tips for Successful Negotiation

-

Always stay polite — never argue.

-

Be realistic; don’t ask for impossible conditions.

-

Show proof of effort (e.g., part payments or savings plan).

-

Ask for written confirmation once an agreement is reached.

Step 7: Get Everything in Writing

Never rely on verbal promises.

Once your lender agrees to the new terms, request a written agreement or updated loan schedule.

This document protects both of you and proves that you’re not avoiding payment.

Keep a copy (printed or digital) in case of future misunderstandings.

Step 8: Stick to the New Payment Plan

Once your repayment extension is approved, follow it strictly.

Pay on or before the new due dates.

Even if the amount is small, consistency builds trust.

If you make all payments on time, your lender might even reward you with lower interest on future loans.

Step 9: Check Your Credit Report

After completing repayment, confirm that your lender updated your status.

You can check your credit report through:

-

Credit Bureau Nigeria

-

Metropol CRB (Kenya)

-

Experian (South Africa)

-

TransUnion (Ghana, Uganda)

This ensures your name stays clean and your credit score improves.

Step 10: Learn and Plan for the Future

Once you finish repaying, take time to reflect.

Ask yourself:

-

What caused the delay?

-

How can I avoid it next time?

-

Should I borrow less or manage my finances better?

Use budgeting apps, set savings goals, and build an emergency fund to avoid future loan stress.

Benefits of Negotiating Loan Repayment Extensions

| Benefit | Explanation |

|---|---|

| Avoids Blacklisting | Keeps your name clean in credit records |

| Reduces Stress | You get time to recover financially |

| Maintains Trust | Builds a good relationship with lenders |

| Improves Credit Score | Shows responsibility and honesty |

| Easier Access to Future Loans | Lenders trust you more |

| Prevents Legal Action | Avoids lawsuits or harassment |

| Financial Peace of Mind | You can focus on rebuilding your finances |

What to Avoid When Negotiating Loan Extensions

Even though asking for an extension is good, some mistakes can ruin your chances.

1. Ignoring Calls or Messages

When you hide from lenders, they assume you’re avoiding payment. Always communicate.

2. Giving False Information

Never lie about your reason. If your lender discovers the truth, they may deny your request.

3. Missing New Deadlines

If you fail to follow the new plan, lenders may blacklist you.

4. Borrowing from Another App to Pay

This creates a dangerous debt cycle. It’s better to negotiate directly than borrow again.

5. Being Rude or Emotional

Always remain calm and professional — lenders are more likely to help polite customers.

Loan Extension vs Loan Restructuring: What’s the Difference?

| Feature | Loan Extension | Loan Restructuring |

|---|---|---|

| Meaning | More time to repay | Changing the entire loan structure |

| Duration | Short-term (30–90 days) | Long-term (months to years) |

| Interest Impact | May slightly increase | May lower or re-adjust interest |

| Suitable For | Temporary cash flow issues | Serious financial hardship |

| Example | Asking for 30 extra days | Changing a 6-month loan into a 12-month loan |

Understanding this helps you choose the right option for your situation.

Real-Life Examples of Successful Loan Extension Negotiations

Example 1: Kenyan Student

Mary, a student at Nairobi University, borrowed KSh 20,000 from a student loan app. Her parents delayed her allowance, so she emailed the lender early.

The lender gave her 45 extra days and waived penalties. She repaid successfully and even got a higher loan next semester.

Example 2: Nigerian Business Owner

Tunde, a Lagos small business owner, borrowed ₦100,000 to restock his shop. When sales dropped, he contacted the lender before the due date.

He negotiated a 2-month extension and paid weekly in smaller amounts. His business recovered, and he avoided blacklisting.

Example 3: South African Worker

Lerato, from Johannesburg, faced medical bills that drained her salary. She contacted her bank early, explained her case, and requested a payment holiday.

The bank approved a 60-day extension with no penalty. Her credit score remained clean.

Tips to Increase Your Chances of Approval

-

Communicate early — Don’t wait for default.

-

Provide proof — Show salary slips, bills, or receipts if needed.

-

Show repayment history — If you have paid before, mention it.

-

Stay professional — Use polite language and proper emails.

-

Follow up regularly — Don’t assume approval; confirm by phone or message.

Legal Rights of Borrowers When Requesting Extensions

You have rights as a borrower, especially in African countries with financial regulations.

Your Rights Include:

-

Right to fair treatment

-

Right to request repayment flexibility

-

Right to privacy (no public shaming)

-

Right to be informed before blacklisting

-

Right to dispute inaccurate reports

If your lender threatens or embarrasses you, report them to:

-

CBN (Nigeria)

-

CRB (Kenya)

-

National Credit Regulator (South Africa)

-

Bank of Ghana

-

Central Bank of Uganda

How to Write a Loan Extension Request Letter or Email

Here’s a simple, professional sample you can use:

Subject: Request for Loan Repayment Extension

Dear [Lender’s Name],

I hope this message finds you well. I am writing to request a short extension for my loan repayment of [Amount], which is due on [Date].

Due to [state reason briefly — salary delay, medical emergency, etc.], I am unable to complete payment as planned. However, I am committed to repaying in full and would like to request an additional [number] days to complete the repayment.

Please let me know if there are any fees or forms I should complete to process this request.

Thank you for your understanding and support.

Sincerely,

[Your Full Name]

[Phone Number]

[Loan Account Number]

Summary Table: Steps to Negotiate Loan Repayment Extensions

| Step | Action | Goal |

|---|---|---|

| 1 | Review loan agreement | Know your rights and terms |

| 2 | Assess finances | Understand what you can pay |

| 3 | Contact lender early | Avoid default or blacklisting |

| 4 | Explain situation | Build trust |

| 5 | Propose new plan | Show responsibility |

| 6 | Negotiate terms | Agree on new timeline |

| 7 | Get written proof | Secure legal protection |

| 8 | Stick to new plan | Maintain good record |

| 9 | Check credit report | Ensure update of status |

| 10 | Plan ahead | Avoid future delays |

Frequently Asked Questions (FAQs)

1. What is a loan repayment extension?

It means getting extra time to repay your loan without penalties or blacklisting.

2. Can every borrower request an extension?

Yes, as long as you contact your lender early and show genuine reasons.

3. Will I pay extra interest if I extend my loan?

Some lenders may charge a small fee, but many waive it if you request politely.

4. Can I still get future loans after an extension?

Yes! Lenders respect borrowers who communicate responsibly.

5. How soon should I ask for an extension?

At least 5–10 days before your due date.

6. What if my lender refuses my request?

Try renegotiating or seek help from a credit counselor or financial regulator.

7. Will extension requests affect my credit score?

No, as long as you repay within the new schedule.

8. Can students request extensions?

Yes, student loan apps and institutions often allow it.

9. What if I can’t pay even after the extension?

Talk again with your lender or consider loan restructuring instead.

10. How do I know if I’ve been blacklisted?

Check your report from a registered credit bureau in your country.

11. Can I negotiate through text or email?

Yes, written communication is better for record-keeping.

Conclusion

Negotiating a loan repayment extension is not a sign of failure — it’s a sign of financial responsibility.

When you act early, communicate clearly, and stay committed, you can fix repayment problems without blacklisting or stress.

Whether you’re a student in Ghana, a worker in South Africa, or an entrepreneur in Nigeria, remember: lenders prefer responsible borrowers who talk instead of hide.

So take control of your finances — follow the steps in this guide, stay disciplined, and rebuild your financial confidence today.