In today’s world, where money matters more than ever, understanding compound interest can change the way students and working-class citizens in Nigeria, Kenya, Ghana, Uganda and South Africa build savings and investment. This guide uses simple, clear English so that even a 10-year-old can follow along, yet it is detailed enough to help you make smarter financial decisions. Let’s get started.

What Is Compound Interest?

Definition of Compound Interest

Compound interest is the interest you earn on both your initial amount of money (which is called the principal) and on the interest that has been added to it over time. In other words, your money grows faster because it earns interest, and then that interest itself earns interest.

Imagine you plant a tree. The tree grows and produces fruit. You then use the fruit’s seeds to plant more trees, and those trees also grow and produce fruit. That’s how compound interest works: your money keeps growing, and that growth generates more growth.

Why It Matters for Students and Working Adults

-

If you are a student in Lagos, Nairobi, Accra or Kampala, saving a little now can lead to more later because of compound interest.

-

If you are working in Port Harcourt, Kampala or Johannesburg, your salary savings or small investments can benefit from compounding and help you prepare for the future.

-

The power of compound interest means time matters: the sooner you start, the more you’ll gain.

-

Understanding how to use it properly can mean the difference between just saving money and making money work for you.

Related Terms You Should Know

-

Principal: The original amount you invest or save.

-

Interest rate: The percentage at which your principal grows.

-

Compounding frequency: How often interest is added (annually, semi-annually, quarterly, monthly, daily).

-

Compound growth: The increase in value because of compounding.

-

Savings interest: What bank pays you for saving money.

-

Investment growth: How your money increases when you invest it and let interest compound.

Simple Interest vs Compound Interest

To understand fully, let’s compare compound interest with simple interest.

Simple Interest: You earn interest only on the principal amount.

-

Example: If you save ₦10,000 at 5% a year with simple interest, you get ₦500 each year, always ₦500, for each year.

Compound Interest: You earn interest on both principal and past interest.

-

Example: If you save ₦10,000 at 5% a year with compounding annually, in year one you get ₦500, so you have ₦10,500. In year two you earn 5% on ₦10,500, so you get ₦525, and so on. Your interest earns interest.

Key differences:

-

With simple interest, growth is linear (same amount each year).

-

With compound interest, growth is exponential (amount increases each year).

-

Over time, compound interest yields much greater returns than simple interest.

This shows why understanding compounding is so important for saving and investing.

How Compound Interest Works Step by Step

Here is a clear, step-by-step guide you can follow to understand how compound interest works in practice.

Step 1 – Identify the Principal

Start by writing down how much money you are going to invest or save. This first amount is your principal.

-

Example: You are a student in Abuja and you decide to save ₦50,000. That ₦50,000 is your principal.

-

Example: You are working in Nairobi and you start an investment of KSh 100,000 – that is your principal.

Check: The larger the principal, the more you can benefit from compounding (given the same interest rate and time).

Step 2 – Choose the Interest Rate

Next, you need to know the interest rate – the percentage at which your money will grow per period (year, month etc.).

-

Example: A bank in Lagos offers 6% interest per year.

-

Example: An investment plan in Kampala gives you 8% per year.

The rate matters: a higher interest rate means faster growth, but higher rates often come with higher risk too.

Step 3 – Decide the Compounding Frequency

Compounding frequency means how often interest is added to your principal and past interest. Common frequencies are:

-

Annually (once a year)

-

Semi-annually (twice a year)

-

Quarterly (4 times a year)

-

Monthly (12 times a year)

-

Daily (365 or 360 times a year)

The more frequent the compounding, the more interest you earn in the same time.

-

Example: If you have 6% per year compounded monthly, you earn interest each month on growing balance.

-

Example: If the same 6% were compounded only once annually, you earn interest once per year.

Step 4 – Calculate and Watch the Growth Over Time

Once you have principal, rate, and frequency, you calculate how your money grows over years. The growth happens because each period you earn interest on a bigger balance (principal plus previous interest). This is compound growth.

You should watch how this works:

-

After 1 year you have principal + interest.

-

After 2 years you earn interest on that bigger balance.

-

After 5, 10, 20 years you might be surprised how much your money has grown.

For a student or worker in Ghana, Nigeria or Kenya, understanding that “my money will grow even while I sleep” can motivate saving earlier and longer.

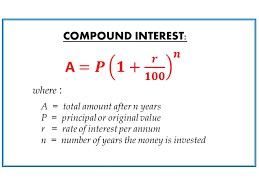

Formula for Compound Interest

Here is the standard formula for compound interest:

A=P×(1+rn)(n×t)A = P \times \left(1 + \frac{r}{n}\right)^{(n \times t)}

Where:

-

A = the amount of money accumulated after t years, including interest.

-

P = principal (initial amount).

-

r = annual interest rate (in decimal form, so 6% = 0.06).

-

n = number of times the interest is compounded per year.

-

t = time the money is invested or saved, in years.

Explanation of Variables

-

P (Principal): Your starting amount (e.g., ₦100,000 or KSh 50,000).

-

r (Interest Rate): Example 5% = 0.05.

-

n (Compounding Frequency): If interest is added monthly, n = 12. If yearly, n = 1.

-

t (Time): How many years you leave the money untouched.

-

A (Accumulated Amount): What you’ll end up with after t years.

Example Calculation (Easy for a 10-Year-Old)

Let’s make this super simple:

-

You save ₦20,000.

-

Interest rate = 5% per year (r = 0.05).

-

Compounded once a year (n = 1).

-

Time = 3 years (t = 3).

Plug into formula:

A=20,000×(1+0.051)(1×3)A = 20,000 \times (1 + \frac{0.05}{1})^{(1 \times 3)} A=20,000×(1+0.05)3A = 20,000 \times (1 + 0.05)^{3} A=20,000×(1.05)3A = 20,000 \times (1.05)^{3} (1.05)3=1.157625(1.05)^{3} = 1.157625

So

A=20,000×1.157625≈23,152.50A = 20,000 \times 1.157625 \approx 23,152.50

Meaning after 3 years you’ll have about ₦23,152.50. That’s more than ₦20,000. The extra ₦3,152.50 is the interest and “interest on interest” working.

If it were compounded monthly (n=12), you’d get a little more by the end of 3 years because interest is added more often.

Real-Life Examples of Compound Interest for Students and Working Class

Here are examples that students and young workers in Nigeria, Kenya, Ghana, Uganda and South Africa can relate to.

Example: Savings in a Nigerian Bank

You are a student in Lagos. You manage to save ₦100,000 this year. A bank offers you 7% per year compounded monthly.

Let’s see:

-

P = 100,000

-

r = 0.07

-

n = 12

-

t = 5 years

A=100,000×(1+0.0712)(12×5)A = 100,000 \times \left(1 + \frac{0.07}{12}\right)^{(12 \times 5)}

You plug numbers and after 5 years you might end up with roughly ₦140,000+ (just an estimate). That’s because each month the interest is added and then interest builds.

What you learn: start early, save regularly, choose a good rate, and allow time for compounding.

Example: Small Investment in Kenya

You are a working adult in Nairobi. You invest KSh 200,000 in a recurring investment account that gives 8% per year compounded quarterly (n = 4). You plan to leave it for 10 years.

-

P = 200,000

-

r = 0.08

-

n = 4

-

t = 10

After 10 years, your money will grow significantly thanks to compounding. It may turn into ~KSh 430,000 or more (depending on specifics). The key: time + rate + compounding help.

Example: Long-Term Growth in Ghana

A teacher in Accra invests GHS 50,000 at 6% per year, compounded annually, for 15 years.

-

P = 50,000

-

r = 0.06

-

n = 1

-

t = 15

After 15 years, because of compounding, you might have around GHS 120,000+. More than double your initial savings.

Why These Examples Matter

-

They show how even modest amounts become larger with time and compounding.

-

They connect to local currencies and local contexts in Africa.

-

They motivate students and working class to start early, save consistent, and pick good savings/investment options.

Advantages of Compound Interest

Understanding the benefits helps you see why it’s such a powerful tool.

-

Money Grows Faster Over Time

Because you earn interest on past interest, not just on the principal. -

Encourages Saving Early

If you start saving young (as a student or new worker), you have more time for compounding to work. -

Passive Growth

Once you set it up (save or invest), your money grows even when you are not actively doing anything — while you study, work, sleep. -

Boosts Investment Returns

Compound interest is one of the main ways investments grow; over years it adds up significantly. -

Helps Beat Inflation

If the interest rate is higher than inflation rate, compounding helps your money keep value or increase in real terms. -

Simple to Understand

With the right formula and steps, you can plan for your future savings and investment growth.

Disadvantages or Risks of Compound Interest

While compound interest is powerful, there are also important caveats and risks you must know.

-

Low Interest Rate Means Slower Growth

If the rate is small (say 2% or 3%) compounding will still grow money, but slowly. -

High Inflation Can Eat Gains

If your country has high inflation (e.g., Nigeria’s inflation rate), the real value of your savings may shrink if your interest rate is lower. -

Compounding Works Both Ways

If you borrow money, compound interest can work against you (you owe interest on interest). -

Fees and Taxes Can Reduce Growth

Some savings/investment accounts come with fees or taxes which reduce the effective growth. -

You Must Leave Money Untouched

Withdrawing early or frequently can reduce the benefit of compounding. -

Risk of Low-Quality Investment Platforms

Especially in countries where regulation may be weaker – you must ensure your bank or investment is safe and credible.

By being aware of these disadvantages you can make smart choices and avoid common pitfalls.

Comparison: Compound Interest vs Simple Interest in Everyday Life

Here is a direct comparison in everyday terms relevant to our audience.

Scenario A: Student Savings in Nigeria

-

You save ₦50,000 at 5% simple interest per year for 5 years.

-

Each year you get ₦2,500 (5% of 50,000). After 5 years you have ₦62,500 (50,000 + 5 × 2,500).

-

-

You save ₦50,000 at 5% compound interest per year (compounded annually) for 5 years.

-

After first year: ₦50,000 + ₦2,500 = ₦52,500.

-

Second year: interest on ₦52,500…, and so on. After 5 years you get higher than ₦62,500 (roughly ₦63,814).

-

-

The difference may not look huge for 5 years, but for 10-15 years it becomes significant.

Scenario B: Small Investment in Kenya

-

You invest KSh 100,000 at 6% simple interest per year for 10 years = KSh 160,000.

-

You invest KSh 100,000 at 6% compound interest per year for 10 years = about KSh 179,000 (because compounding).

-

The difference grows larger the more years you wait.

Why This Comparison Matters

-

It helps you see “interest on interest” effect.

-

You learn that for long-term savings, compounding is far more powerful than simple interest.

-

For students and working adults who may think “I’ll just deposit and forget”, understanding the type of interest is important in choosing the right account/investment.

Tips to Make the Most of Compound Interest for Students and Workers

Here are practical tips tailored for you in Nigeria, Kenya, Ghana, Uganda, South Africa or any similar country.

-

Start Early

The sooner you start saving/investing, the more time compounding has to work. Even small amounts count. -

Save Regularly

Try to deposit money consistently (monthly or quarterly) rather than just once. This helps build your principal and benefits compounding. -

Choose Good Interest Rates

Look for savings or investment accounts with higher rates and favourable compounding frequency (e.g., monthly vs annually). -

Let Money Stay in for the Long Term

The longer you leave money untouched, the more you benefit from “interest on interest”. -

Reinvest Your Interest

Don’t withdraw the interest; leave it in so it can also earn interest. -

Understand Fees, Taxes, and Inflation

Make sure that the rate you earn is after costs, and that you consider inflation’s effect on your real returns. -

Use Reliable Banks or Investment Platforms

Especially in countries with less stable financial systems, pick banks/investment firms regulated and trusted. -

Use Online Tools and Calculators

Use a compound interest calculator (there are many free online) to project your growth, so you can set goals. -

Start Small if You Can’t Save Big

Even if you save a small amount like ₦5,000 or KSh 1,000 monthly, over years compounding will help. -

Educate Yourself

Keep learning about other tools such as mutual funds, bonds, fixed deposits etc., that use compounding.

Common Mistakes to Avoid with Compound Interest

Here are some of the pitfalls many students and workers fall into—and how to avoid them.

-

Mistaking simple for compound interest: Always check whether the rate is simple or compounded.

-

Not checking the compounding frequency: 6% annually vs 6% monthly compounding is different.

-

Withdrawing early: Taking money out early stops compounding.

-

Not accounting for inflation: A high nominal rate might still lose value if inflation is higher.

-

Ignoring fees and charges: Some accounts charge maintenance or hidden fees that reduce your effective return.

-

Leaving money idle at very low rates: If you save at a very low rate (say 1% when inflation is 10%), you’re losing purchasing power.

-

Putting all your savings into risky high-rate schemes without checking safety: High rates can mean high risk.

-

Not taking advantage of time: Many people wait until later in life to start saving; the earlier you begin, the better.

-

Relying solely on interest earnings: You should still build a diversified savings/investment plan; compound interest is one tool.

-

Assuming compound interest will make you rich overnight: It grows slowly at first; compounding shines over long periods.

Summary Table

Here is a quick summary to help you review what we’ve covered:

| Topic | Key Points |

|---|---|

| Definition of Compound Interest | Interest on principal + interest already earned |

| Principal | Starting amount you invest or save |

| Interest Rate | Percentage at which money grows |

| Compounding Frequency | How often interest is added (annually, monthly, etc.) |

| Formula | A=P×(1+r/n)n×tA = P \times (1 + r/n)^{n \times t} |

| Simple vs Compound | Compound grows faster; simple grows linearly |

| Real-Life for African Students | Examples in Nigeria, Kenya, Ghana, Uganda using local currency and context |

| Advantages | Faster growth, passive income, early start, inflation hedge |

| Disadvantages / Risks | Low rate, inflation, fees, early withdrawal, risk if borrowing |

| Best Practices / Tips | Start early, reinvest, choose good rate, check fees, use trusted banks |

| Common Mistakes | Confusing rates, ignoring inflation, withdrawing early, high-risk schemes |

Frequently Asked Questions (FAQs)

Here are over 10 common questions (and clear answers) about compound interest, tailored for students and working-class in Africa.

1. What is compound interest and how is it different from simple interest?

Compound interest is when you earn interest on both your original money and on the interest you’ve already earned. Simple interest is interest only on the original amount. Over time compound interest grows faster.

2. What does ‘compounded monthly’ or ‘compounded annually’ mean?

It means how often the interest is added to your account. If it’s “compounded monthly”, interest is added each month and then you earn interest on that new amount each month. If annually, only once per year.

3. Can I use compound interest for savings in Nigeria or Kenya?

Yes. Many banks and investment firms in Nigeria, Kenya, Ghana, Uganda, South Africa offer savings or investment accounts where interest compounds. Always check the terms (rate, frequency, fees).

4. Is starting with a small amount still useful?

Definitely yes. Even a small amount saved regularly will grow thanks to compound interest. Starting small is better than not starting at all.

5. How long do I need to wait for compound interest to make a big difference?

The longer you wait, the more difference it makes. For example, over 10 or 15 years you’ll see strong growth. Over 2–3 years the growth will be smaller.

6. What rate of interest should I look for?

Look for a rate that is above inflation and comes with frequent compounding (monthly or quarterly) and low fees. Compare between banks/investments in your country.

7. Does compounding work if I withdraw the interest every time?

It works less effectively if you withdraw interest. The power of compounding grows when you leave the money (principal + interest) invested so interest keeps earning interest.

8. What’s the effect of inflation on compound interest?

Inflation means money loses purchasing power over time. If your interest rate is lower than inflation, your real value might shrink even if the nominal amount grows. So aim for rate > inflation.

9. Are there risk-free compound interest accounts?

There are accounts with low risk (like savings bank accounts) but usually lower rates. Higher rates often come with more risk. Always check safety of the bank/investment firm.

10. Can compound interest work against me?

Yes—if you borrow money and interest compounds, you may end up owing more and more. Also, if you invest at very low rates or in risky schemes, compounding may not help as much.

11. How often should I deposit money to benefit most?

If possible, deposit regularly (monthly or quarterly) rather than once. Regular deposits increase your principal faster and give compounding more to work on.

12. What is “effective annual rate” (EAR) and why is it important?

The effective annual rate is the real rate you earn or pay after factoring in the effect of compounding frequency. It helps you compare accounts that compound differently (e.g., monthly vs annually).

13. Can students benefit from compound interest?

Yes. If you save money even while studying, the money will grow. The early you start—while you’re a student—the more you gain later when you enter the workforce.

14. How can I use compound interest to reach financial goals?

Think of a goal (e.g., buying a car, starting a business). Calculate how much to save and how many years, pick a rate and compounding frequency, use the formula or calculator and then start regularly saving to reach the goal.

Conclusion

Understanding compound interest is one of the most valuable financial lessons you can learn—especially as a student or working professional in Nigeria, Kenya, Ghana, Uganda or South Africa. By knowing how your principal, interest rate, compounding frequency and time work together, you can set up your money to grow smarter. Starting early, picking the right savings/investment option, reinvesting interest and avoiding common mistakes will help you make the most of the power of compound interest.

Save this guide, refer back to it, use it when you choose bank accounts or investments. Let your money work for you rather than just sitting inactive.